Industry organization SEMI has released a report from analyst agencies Semiconductor Manufacturing Monitor and TechInsights on the development of the global semiconductor industry in the fourth quarter of 2024. Most key segments are experiencing strong growth. Forecasts for 2025 are cautiously optimistic, as macroeconomic uncertainty may hinder near-term growth, despite momentum driven by strong AI-related investments.

Image source: Global Foundres

The SMM report provides end-to-end data on the global semiconductor manufacturing industry. It highlights key trends based on industry metrics including capital equipment, manufacturing capacity, semiconductor and electronics sales, and a capital equipment market forecast. The report also provides biennial quarterly data and a semiconductor supply chain forecast.

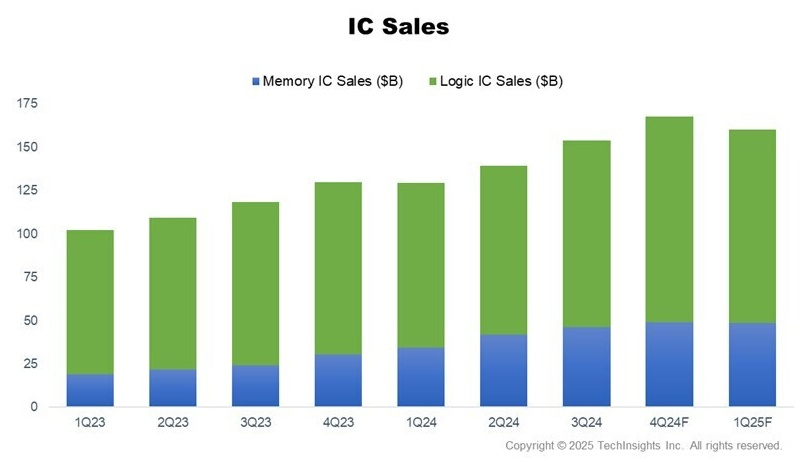

After declining in the first half of 2024, electronics sales have recovered and posted a 2% annual growth. Electronics sales grew 4% year-over-year in the fourth quarter of 2024 and are expected to increase 1% in the first quarter of 2025. Integrated circuit (IC) sales grew 29% year-over-year in the fourth quarter. They are expected to grow 23% in the first quarter of 2025, driven by the ongoing AI boom.

Image source: Semiconductor Manufacturing Monitor report

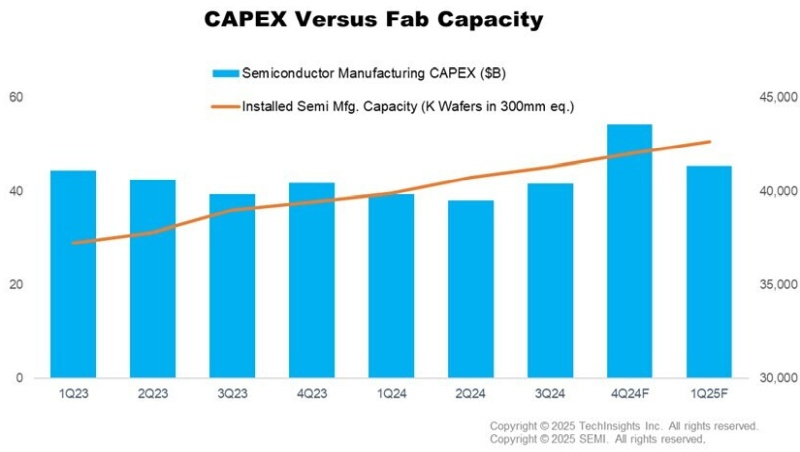

Capital expenditure in the semiconductor industry declined in the first half of 2024 but then rebounded sharply in the fourth quarter, resulting in a 3% year-over-year increase. Memory led the investment, with spending in the fourth quarter of 2024 up 53% sequentially and 56% year-over-year. Capital expenditure in other semiconductors increased 19% sequentially and 17% year-over-year.

Total capital expenditure is expected to increase 16% year-on-year in the first quarter of 2025, driven by investments in high-bandwidth memory (HBM) capacity for AI deployment.

Wafer fabrication equipment (WFE) spending increased 14% year-on-year and 8% quarter-on-quarter in Q4 2024, with investment in the sector expected to reach around $26 billion in Q1 2025. Chinese investment played a significant role in this market, but began to taper off toward the end of the year.

In Q4 2024, installed wafer fab capacity exceeded a record 42 million wafers per quarter worldwide (300mm wafer equivalent), and is expected to grow to 42.7 million wafers per quarter in Q1 2025. Contract and logic fab capacity continues to grow, growing 2.3% sequentially in Q4 and is expected to grow 2.1% in the current quarter of 2025, driven by capacity expansion in advanced process technologies.

In addition, internal hardware costs increased significantly in Q4 2024. The testing segment grew 5% QoQ and an impressive 55% YoY, while the assembly and packaging segment grew 15% YoY. In Q1 2025, both segments are expected to show similar QoQ growth of between 6% and 8%.

«“Despite seasonality and macroeconomic uncertainty challenges, the momentum of AI investment continues to fuel expansion in key segments including memory, capital expenditures, and wafer fab equipment,” said Clark Tseng, senior director of market analysis at SEMI. “Looking ahead to 2025, the industry remains cautiously optimistic, with robust growth prospects driven by continued demand for high-performance computing and data center construction.”

«We expect stronger performance in the second half of the year, […] semiconductor sales will remain flat in the first half, followed by strong double-digit growth in the second half of the year, said Boris Metodiev, director of market analysis at TechInsights. “Inventory issues remain for discrete, analog, and optoelectronic device makers that will need to be addressed before we can expect growth to resume across the board.”