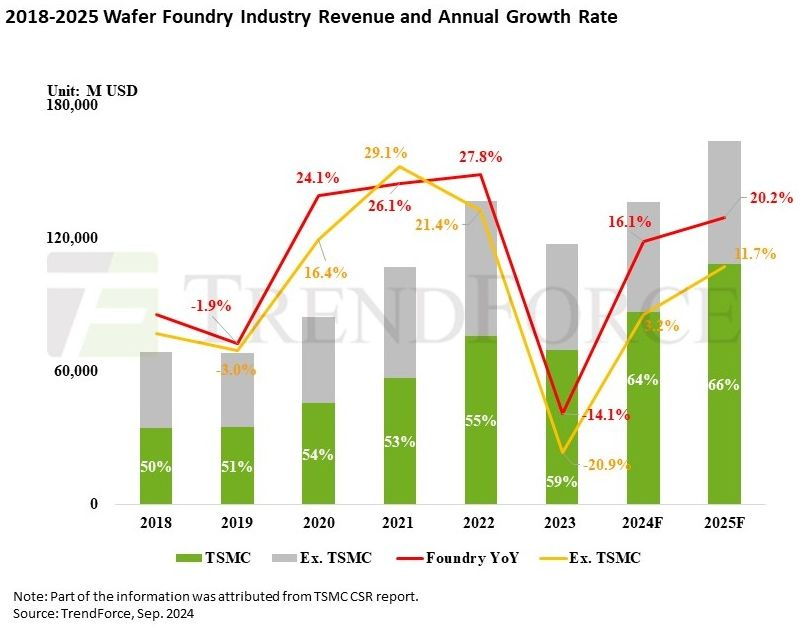

At the end of this year, according to TrendForce analysts, the revenue of contract chip manufacturers will grow by 16%, which can be considered a good rebound after last year’s drop of 14%. Next year, revenue growth for contract chip manufacturers will exceed 20%, according to experts.

Image source: GlobalFoundries

However, it is difficult to talk about an improvement in the demand situation in consumer markets. This year, the equipment utilization rate on lines for the production of not the most advanced chips has dropped below 80%, which cannot be considered an optimal level from an economic point of view. Only lines for the production of chips using technological processes from 5 to 3 nm inclusive were fully loaded, and this state of affairs will continue next year, which cannot be guaranteed for the consumer market.

As noted in the TrendForce report, already in the current half of the year, the markets for automotive electronics and industrial automation will begin to recover after the correction of inventories, and this process will continue in 2025. The boom in artificial intelligence systems is driving the number of silicon wafers processed by the industry. This will largely contribute to the fact that contract chip manufacturers’ revenue will grow by 20% next year. If we exclude TSMC, the leader in market share, from this sample, the growth will be limited to 12%, but even in this case it will be higher than the level of the previous year.

Image source: TrendForce

Next year, the 3nm process will become the main process for the production of advanced computing components, including central processing units for PCs and smartphones, but computing accelerator chips will remain on 5nm and 4nm process technologies. By the second half of the year, demand for 6nm and 7nm chips used in smartphones to operate in wireless communication networks will begin to grow. According to TrendForce, in 2025 the range of technological processes from 7 to 3 nm will form up to 45% of the revenue of contract chip manufacturers worldwide.

High demand for chip packaging services using the 2.5D class layout has led to continued shortages throughout the current and previous years. TSMC, Samsung and Intel are trying to expand their core production capacities. Revenue from the provision of such services will grow by more than 120% by the end of 2025. True, for now they will form no more than 5% of the revenue of contract manufacturers, but this share will gradually grow.

The restoration of demand in the consumer market, as TrendForce experts hope, will allow contract manufacturers by the end of 2025 to increase the utilization rate of lines for processing silicon wafers using mature technical processes to a level of more than 70%, although now in most cases it does not exceed 60%. New enterprises using technological processes in the range from 28 to 55 nm will also be commissioned. Prices for services for the production of chips of this class may decrease as a result of the emergence of new capacities. Contract market participants will have to deal with the high costs of introducing advanced equipment and macroeconomic uncertainty.