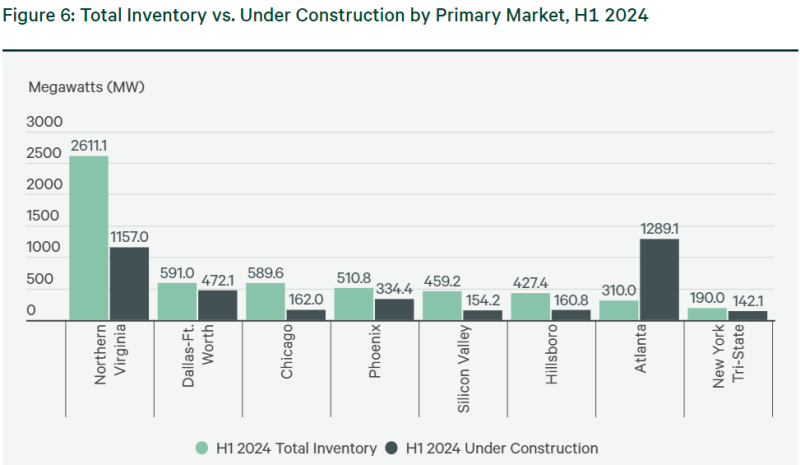

According to a CBRE study, the number of data centers under construction is growing rapidly due to the boom in AI systems, The Register reports. At the same time, as reported in the report, in the leading markets of North America over the past year, growth was about 70%, reaching a record 3.87 GW. Among the fastest-growing regions is Atlanta, where data center construction volumes grew 76% year-over-year to approximately 1.3 GW. In Texas (Austin and San Antonio), 463 MW of new data center capacity is being built, more than four times more than a year earlier.

Rapid expansion is hampered by the lack of available data center electricity and the long time it takes to create the critical infrastructure necessary to put facilities into operation. However, even when these facilities become operational, only about 20% of their resources will be available to ordinary users; about 80% of the 3.87 GW has already been reserved by hyperscalers, cloud providers and data center operators renting out AI accelerators.

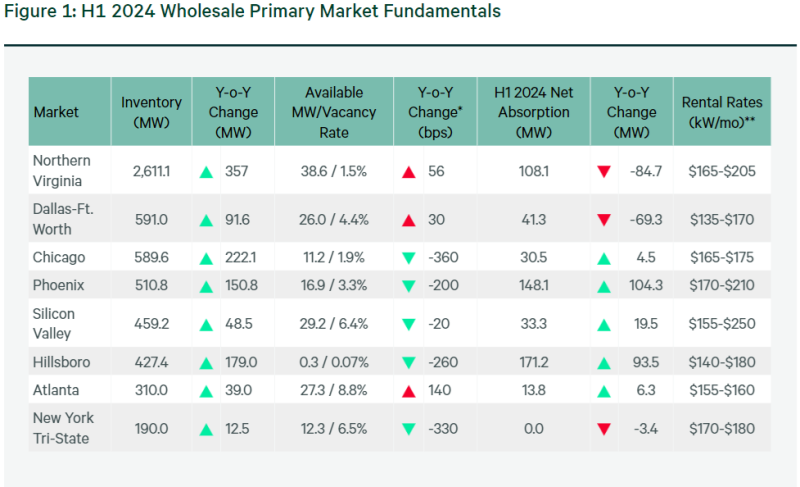

CBRE reports that data center capacity in key markets grew by 10% in the first half of 2024, with 1.1 GW of facilities operational last year. However, the availability of capacity is still limited, since on average only 2.8% of resources are free in these regions. However, if you wish, you can turn to less popular areas like Central Washington, Minneapolis, Houston or Denver, since 10% are free in secondary markets in North America.

Image Source: CBRE

The lack of new data centers and high demand is leading to price increases, although not as fast as last year. Average monthly demand is 250–500 kW in key markets, growing 7% in Q1 2024 to $174/kW per month. Rents are expected to continue rising in the second half of the year, largely due to rising construction and equipment costs. The trend is also driven by the use of more resource-intensive AI accelerators. For example, the consumption of one NVIDIA Blackwell accelerator can reach 1200 W; it was originally designed for the use of LSS.

According to CBRE experts, as a result, the construction of new data centers will only become more expensive. On the other hand, poorly equipped old data centers that are not ready to work with modern accelerators may become more accessible to less demanding users. It is predicted that secondary markets in Northern Indiana, Idaho, Arkansas and Kansas, due to the abundance of cheap land and energy, could become new centers of data center development.

Image Source: CBRE

As for energy, the shortage of transformers, switches and generators will continue for another four years, which cannot but affect the construction time of data centers. CBRE notes that clients wishing to receive the required capacity on time should enter into agreements 2-4 years before the expected commissioning of facilities.