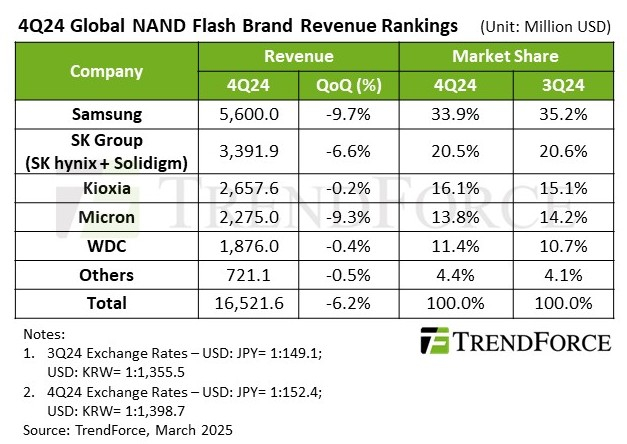

In the fourth quarter of last year, the NAND memory market was under pressure as PC and smartphone makers continued to try to optimize their inventory, according to TrendForce. Average flash memory prices fell 4% sequentially last quarter, while shipments fell 2%. This led to a 6.2% decline in revenue for market participants to $16.52 billion.

Image source: Micron Technology

The first quarter is traditionally a low season for the solid-state memory market, and this year is no exception, even taking into account the manufacturers’ increased attempts to reduce their product supply volumes. Replenishment of warehouse stocks has slowed in most key markets, including the server segment. According to the results of the first quarter, the revenue of flash memory suppliers may consistently fall by 20%. It will be possible to talk about the recovery of the NAND memory market only by the results of the second half of this year, if everything goes according to plan.

The NAND market leader remains Samsung Electronics, which consistently reduced its revenue by 9.7% to $5.6 billion in the last quarter, mainly due to the consumer electronics segment. In the future, the company plans to focus on promoting solid-state drives in the corporate sector. In any case, Samsung still controls 33.9% of the global NAND market.

In second place is SK Group, which combines the classic SK hynix business and assets inherited from Intel, which are now present on the market under the Solidigm brand. Hopes for growth in shipments did not come true for this manufacturer last quarter, as a result of which revenue fell sequentially by 6.6% to $3.39 billion. For this South Korean supplier, the priority is to serve the needs of the AI infrastructure segment.

Third-placed Kioxia saw its business show relative stability in the fourth quarter, as setbacks in the PC and smartphone segments were offset by strong demand for enterprise SSDs. The company’s revenue for the period fell sequentially by just 0.2% to $2.66 billion. Kioxia’s market share actually increased from 15.1% to 16.1%.

In the case of Micron Technology, high demand for enterprise SSDs failed to offset the decline in the consumer segment, with revenues down 9.3% to $2.28 billion. At the same time, Micron’s market share is not that far behind Kioxia’s: 13.8% versus 16.1%. This year, Micron plans to reduce capital expenditures in the NAND segment and focus on producing solid-state drives with a capacity of over 60 TB for enterprise customers.

Western Digital and its SanDisk brand managed to keep revenue roughly in line with the third quarter of last year, as solid-state memory for consumer SSDs sold better than expected in the fourth quarter. Even with falling prices, revenue was down just 0.4% to $1.9 billion. SanDisk could strengthen its position in the PC SSD market this year, as the vendor currently holds 11.4% of the NAND market together with Western Digital. Other solid-state memory makers outside the top five account for no more than 4.4% of the global market in terms of revenue.