AMD is considered the largest NVIDIA competitor in the accelerators market that are used to teach artificial intelligence systems, but as the dynamics of the Red shares shows, investors are not sure that the company is able to cope with this role, writes Bloomberg.

Image source: amd.com

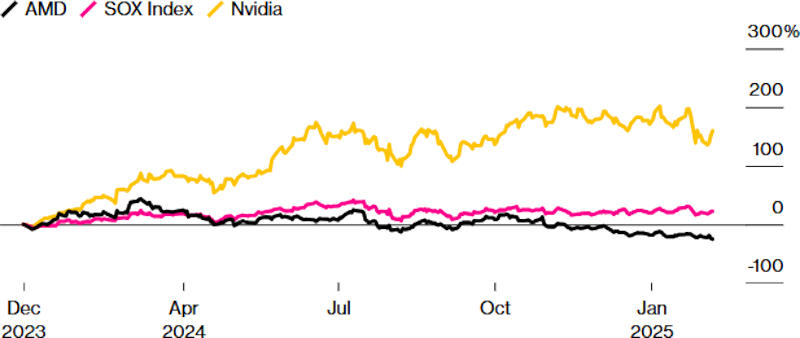

Now AMD securities have been at the lowest level since November 2023 – compared to the end of 2023, they fell by 25 %. For comparison, the Philadelphia Stock Exchange Semiconductor Index indicator has increased by more than 20 %over the same time, and NVIDIA shares went up by 160 %. Only on the eve of February 7, 2025, AMD shares lost 0.9 %in price. The reason for this was the excessive caution of the CEO of Lisa Su (Lisa Su)-during the quarterly report, it refrained from a separate annual forecast for and trains, which are considered a key product. Thus, she did not give a catalyst for financial development for the next six months and transferred investments to AMD into the category of “dead money”, investors complained. The situation aggravated the situation that the company previously talked about income in the AI sector, so that mysterious silence this time caused fears that NVIDIA was too much ahead of all competitors, and AMD may have difficulties with the implementation of its chips for AI.

Image Source: Bloomberg.com

Otherwise, the quarterly report is evaluated as positive: the company showed the revenue above the expected and gave an optimistic general forecast. Dr. Su noted that sales of and accelerators in the first half of 2025 will remain approximately at the level of the second half of 2024. The situation may change for the better in the middle of the year, when the AMD releases an accelerator of the new generation – this attracted the attention of investors who are waiting for the linear growth of the company, which, according to AMD management, will continue in the coming years. But Citi lowered the AMD rating and was not alone in this: Bank of America, HSBC Holdings and Melius Research pointed out the complex nature of competition with NVIDIA. According to IDC, the “green” in the III quarter belonged to 89 %of the global server graphics market, while AMD got only 10.3 %, and Intel only 1.1 %. Even the sensation of the Chinese Deepseek, which achieved significant results at minimal costs, did not save the situation: large companies still decided to double the costs of AI – only Alphabet prepared $ 75 billion.

But investors do not consider the AMD position even hopeless. NVIDIA and Broadcom are unlikely to satisfy the demand of the entire market, and if AMD increases a share of at least 15 %, its income will be significant, they reason. But after the publication of the quarterly report, analysts reduced the predicted AMD indicators: 15 % by net profit and 0.4 % of revenue. This year, as expected, the company’s incomes will grow by 24 %, and net profit – more than three times. Next year, growth will slow down: revenue will increase by 21 %, net profit – by 46 %. This means that the shares are traded at a price of less than 23 times the estimated profit-35 % lower than the average target price indicated by analysts. That is, the worst for AMD in the stock market is probably already behind.