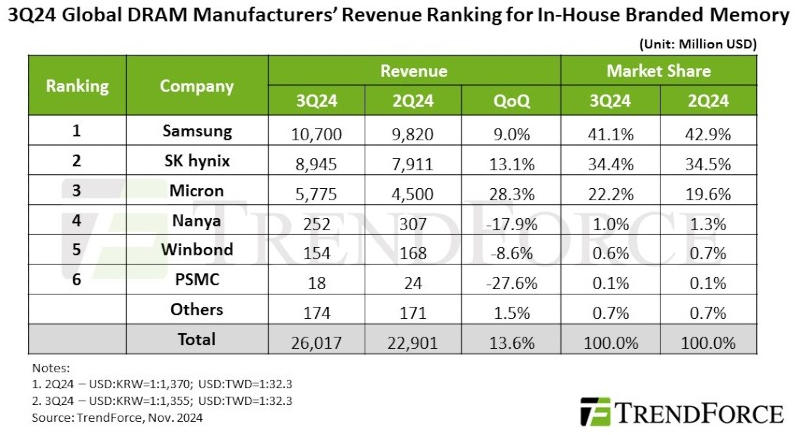

The total revenue of global manufacturers of DRAN RAM chips in the third quarter of 2024 amounted to $26.02 billion, which is 13.6% more than the previous quarter, TrendForce analysts reported. The growth is driven by strong demand for DDR5 and HBM memory for data centers – a trend that was not broken by either a decrease in LPDDR4 and DDR4 supplies due to inventory reductions from Chinese smartphone manufacturers, or the expansion of capacity from Chinese DRAM manufacturers.

Image source: samsung.com

The average selling price (ASP) continued the upward trend seen in the previous quarter; contract prices rose 8% to 13%, and HBM accelerated the trend by displacing conventional DRAM production. For the fourth quarter, analysts are forecasting quarterly growth in overall DRAM bit shipments, although strong HBM production is expected to continue to weigh on conventional DRAM production. Chinese suppliers have begun expanding capacity, which could prompt PC and smartphone makers to aggressively clear inventory and purchase cheaper DRAM. As a result, contact prices for conventional DRAM will begin to decline.

Rising contract prices for DRAM for PCs and servers in the third quarter increased the revenues of the three largest memory manufacturers. First place was retained by Samsung, whose revenue amounted to $10.7 billion – 9% more than the previous quarter. Due to the strategic reduction in LPDDR4 and DDR4 inventories, bit shipments remained at the same level as the previous quarter. SK hynix reported revenue of $8.95 billion – second place and growth of 13.1% quarter-on-quarter. The company increased shipments of HBM3e, but due to weak sales of LPDDR4 and DDR4, bit shipments fell 1-3% quarter-on-quarter. Micron’s revenue rose 28.3% to $5.78 billion due to strong growth in server DRAM and HBM3e shipments, with bit shipments up 13% in the quarter.

Image source: trendforce.com

Revenue from Taiwanese suppliers fell in the third quarter, falling significantly behind the top three brands. Nanya Technology’s bit shipments fell by more than 20% due to weakening demand for consumer DRAM and increased competition in the DDR4 market from Chinese manufacturers. Due to the power outage incident, the company’s operating profit decreased from -23.4% to -30.8%. Winbond’s revenue fell 8.6% quarter-on-quarter to $154 million as demand for consumer DRAM fell and bit supplies declined. PSMC reported a 27.6% decline in revenue from its own consumer DRAM production; But taking into account revenue from semiconductor production, the company’s total revenue from sales of DRAM increased by 18% – this is due to the constant replenishment of inventories from customers for semiconductor production.