TSMC’s third-quarter results released today encouraged investors, as the company’s revenue rose 36% to $23.5 billion and net income beat expectations with a 54.2% increase. Moreover, the company left its capital expenditure forecast for the full year at the existing level, and raised its revenue forecast to a level corresponding to an increase of 30%.

Image source: TSMC

Let us recall that three months ago TSMC hoped to increase annual revenue by 25% compared to 2023, so the improved forecast for the first three quarters of this year indicates the company’s optimism about the dynamics of the key indicator. TSMC’s net income in the third quarter rose 54.2% year-on-year to $10.1 billion, significantly exceeding analysts’ expectations. Quarterly revenue rose 39% in Taiwanese currency terms, but growth was capped at 36% in U.S. dollar terms, although that figure was hardly moderate. TSMC’s net profit margin for the year increased from 54.3% to 57.8%. The operating profit margin increased from 41.7 to 47.5%, and operating profit itself increased by 58.2% to $11.23 billion. The company explains the improvement in these indicators both by successful measures to reduce costs and by an increase in the conveyor utilization rate.

As noted in TSMC’s quarterly reports, in annual comparison, the company’s processing volumes of silicon wafers in 300-mm equivalent increased by 15% to 3.34 million pieces. The company’s capital expenditures in the third quarter increased slightly sequentially to $6.4 billion. The range of capital expenditures for the full year was narrowed at the lower limit, from $28 to $30 billion, but the upper limit remained at $32 billion. This was a good signal for investors, because they were worried that rising costs would undermine the company’s business profitability. Over the three quarters of this year, TSMC managed to spend $18.53 billion on capital needs. Therefore, in the time remaining until the end of the year, it can spend up to $13.5 billion. Next year, the company expects to increase capital expenditures, that is, it is ready to spend on these needs are at least $32 billion.

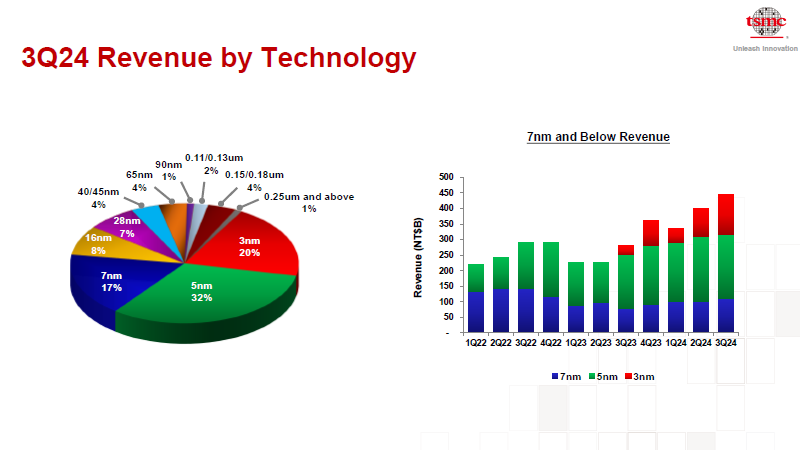

Consecutive revenue growth of 12.8% in the third quarter was driven, as TSMC notes, by strong demand for components for smartphones and AI systems produced using 3nm and 5nm technologies. The share of TSMC’s revenue from the sale of 3-nm components increased over the year from 6 to 20%, but the 5-nm process technology began to lose ground, since a quarter earlier it still provided 35% of TSMC’s revenue, but has now dropped to 32%. Also considered cutting-edge, the 7nm process maintained a stable 17% of revenue for the second quarter in a row. In total, advanced technologies accounted for 69% of TSMC’s revenue in the third quarter. This is significantly higher than historical indicators, which indicates the growing market specialization of the company, since it is one of the few capable of offering services for the production of chips using advanced technologies in significant quantities to a variety of clients.

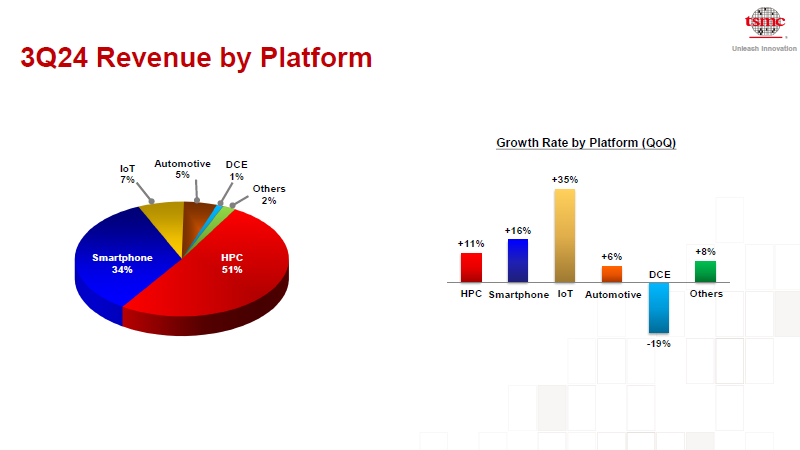

It is noteworthy that TSMC received only 51% of revenue from the sale of components for high-performance computing in the third quarter, while in the previous quarter this share reached 52%. Most likely, this can be explained by the advance nature of the release of products that will hit the market in the third quarter. Seasonal trends also explain the consistent increase in the share of TSMC’s revenue from the sale of smartphone components from 33 to 34%. At the same time, a year ago this figure reached 39%, so we can talk about both stagnation in the smartphone market and more active development of the market for high-performance computing components. A year ago, the latter’s share in TSMC’s revenue did not exceed 42%, but has now grown to 51%. This segment also includes solutions for artificial intelligence systems.

However, if revenue in the HPC segment consistently grew by only 11%, then the smartphone segment added 16%, and the Internet of Things by 35%. Even so, the IoT segment accounts for only 7% of TSMC’s revenue, down from 9% a year ago. The automotive segment posted a stable growth rate of 5%, and in monetary terms its revenue increased sequentially by 6%. In the consumer electronics segment, TSMC’s revenue declined sequentially by 19%. The company’s statistics also included the “other” item, which in the third quarter was responsible for 2% of total revenue and consistently increased it by 8%. A year ago, this item included 3% of revenue.

Geographically, North America is inexorably absorbing an increasingly larger portion of TSMC’s revenue. If a year ago the region’s share did not exceed 69%, now it has grown to 71%, and in the second quarter there was a drawdown to 65%. China is forced to lose ground because of all TSMC’s products, it only has access to the range produced using mature technologies, and this allows the country to lay claim to only 11% of TSMC’s total revenue. A year ago, China’s share reached 12%, but in the second quarter it jumped to 16%.

TSMC CEO C.C. Wei stressed at the quarterly earnings conference that components for AI systems are in high demand, and the industry is only at the beginning of a long growth cycle. Revenue from the sale of server AI chips will more than triple this year, and TSMC will account for about 14–16% of total revenue.

If we talk about the demand for semiconductor components in general, it has stabilized after a long decline and is beginning to grow. For the current quarter, the company expects revenue to range from $26.1 billion to $26.9 billion, which in the center of the range is higher than the $24.9 billion included in third-party forecasts.