Nvidia’s quarterly report stands out in the financial statistics calendar, but that’s not the only thing that attracts increased attention to it. For several quarters in a row, the company’s revenue has been growing at an accelerated pace, fueled by demand for components for artificial intelligence systems. Last quarter, Nvidia increased its overall revenue by 94%, and its server computing segment grew by 132%.

Image source: NVIDIA

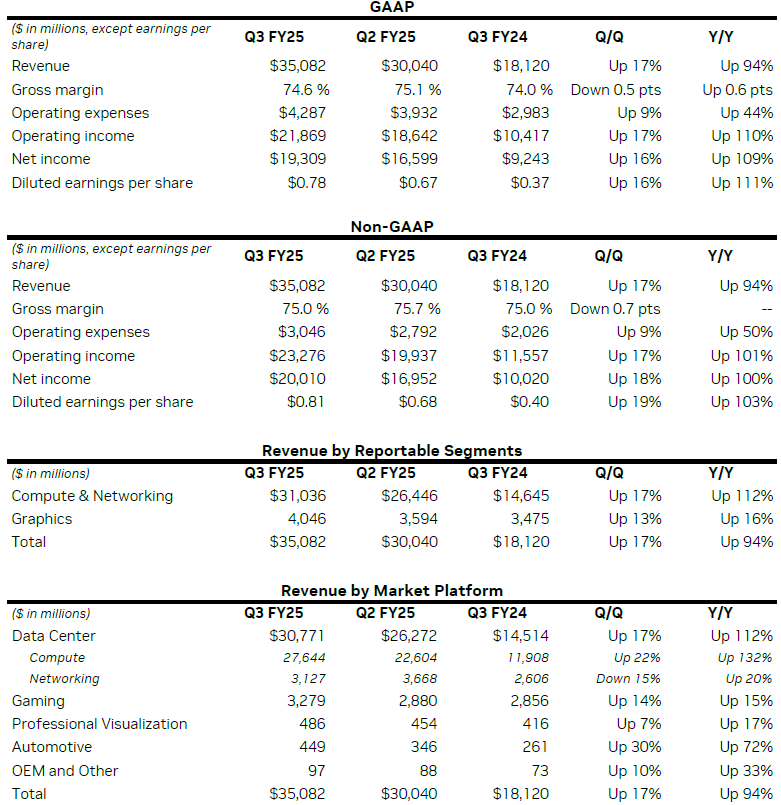

With revenue of $35.08 billion for the quarter as a whole, Nvidia beat the expectations of investors, who on average expected $33.16 billion. Specific earnings per share of 81 cents were also higher than the 75 cents expected. Moreover, in the current quarter, Nvidia expects to earn an average of $37.5 billion, and this amount is also higher than the $37.08 billion forecast by analysts. In any case, investors have reasons for disappointment, because if Nvidia expects growth this quarter revenue by approximately 70%, whereas a year ago it was 265%. The company’s revenue growth rate is slowing down, and the fixation of such expectations caused Nvidia’s share price to fall by 2.5% after the publication of the report.

If we look at the results of the third quarter, then Nvidia’s revenue managed to grow by 94% to $35.08 billion, but even in this case, the growth rate is lower than in the three previous quarters, when they were 122%, 262% and 265%, respectively. One way or another, Nvidia shares have almost tripled in price since the beginning of the year, and the current correction cannot be considered serious. The company is the most expensive among public ones; this status is now not so easy to challenge.

The company’s net income in the third quarter increased by 100% to $20.01 billion, and operating income increased by 101% to $23.3 billion. The profit margin increased year-on-year and remained unchanged at 75%. However, the company’s operating expenses also increased by 50% to $3.05 billion. Specific earnings per share increased by 103% to $0.81.

The engine of Nvidia’s revenue, as you might guess, remains the server segment. Overall, it allowed the company to increase core revenue by 112% to $30.8 billion. In other words, the company received 88% of its revenue in the third quarter in the server segment. Analysts expected an amount of $28.82 billion, if we talk about the server segment separately. However, of the indicated $30.8 billion, approximately $3.1 billion came from revenue from the sale of telecommunications equipment, and only $27.64 billion in pure form relates to accelerators and server processors. In this area, Nvidia’s revenue grew by 132% year-on-year.

Anticipating questions about possible supply problems with Blackwell’s generation of accelerators, CFO Colette Kress said customers have already received about 13,000 samples of such accelerators. CEO Jensen Huang emphasized that Blackwell is in the mass production stage. All of Nvidia’s major customers have received Blackwell samples and are working hard to install them in their data centers as quickly as possible. The company still expects to generate several billion US dollars in revenue from Blackwell shipments in the fourth quarter, and will scale it up in the first quarter. Last quarter, the company managed to significantly increase supplies of H200 accelerators of the Hopper generation.

Inevitably, a discussion of recent rumors about overheating of Blackwell family components in NVL72 server racks forced the company founder to deny the existence of such problems: “There are no difficulties with our liquid-cooled Grace Blackwell systems. Engineering work is not as easy as all our activities, but we are in good shape.” Microsoft and CoreWeave are already installing these systems for their own needs. Colette Kress added that Blackwell’s accelerators will initially provide profit margins in the region of just over 70%, but this will increase later as supply volumes increase. By the middle of next year it could return to around 75%. Colette Kress emphasized that changes to the photomask for making Blackwell chips have been successfully made, and this will reduce the level of defects in production.

Nvidia’s CFO admitted that demand outstrips supply for both Hopper and Blackwell, and the latter will continue to do so for several quarters of fiscal 2026, which the company’s calendar begins in February 2025. Huang added that in order to increase Blackwell’s production volumes, the company’s partners will have to commission new production lines, this will increase the level of product yield and reduce cycle times, ultimately increasing production volumes.

Nvidia’s gaming business performed better than expected ($3.03 billion), showing revenue growth of 15% to $3.28 billion. The most surprising thing is that sales volumes of not only GeForce RTX 40 series gaming GPUs for laptops, but also components for Nintendo game consoles increased Switch, which are now at the end of their life cycle.

The automotive electronics segment added 72% to $449 million in revenue, largely due to demand for chips for autopilot systems. Components for robotic systems are included in the same income item. The professional visualization segment, which describes sales of Quadro family graphics adapters, increased 17% year-on-year to $486 million. The OEM segment grew by a third, but to a modest $97 million.

In general, if Nvidia’s revenue is divided between computing and telecommunications components, on the one hand, and graphics solutions as such, then in the first case it amounted to $31.04 billion, and in the second it was limited to $4.05 billion at the end of the third quarter.

When Nvidia founder Jensen Huang was asked at a reporting conference about the possible impact of increased customs duties that Donald Trump threatens to introduce in the United States, the head of the company only expressed his readiness to come to terms with the decision of the new administration and support such a decision.