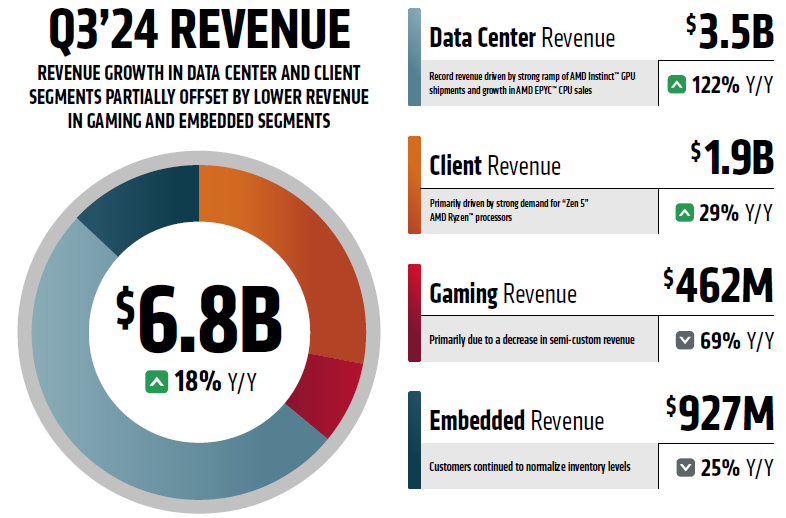

Last night, AMD reported revenue growth of 18% to $6.82 billion, which was higher than analysts’ expectations, and specific earnings of 92 cents per share exactly matched their earlier forecast. However, AMD expects revenue of $7.5 billion for the current quarter, which was worse than market expectations and represents a 22% year-over-year decline.

Image source: AMD

These indicators became the main impetus for the decline in the AMD stock price by 7.6% after the close of the main trading session. Even CEO Lisa Su’s announcement that data center revenue was doubling for the second quarter in a row didn’t help. To be more precise, in the last quarter it grew by 122% year-on-year to $3.55 billion. Accordingly, AMD receives more than half of its revenue in this segment. AMD’s operating profit in the server segment grew by 240% year-on-year to $1.04 billion. The operating profit margin increased from 19 to 29%. The head of the company promised that deliveries of serial computing accelerators Instinct MI325X will begin in the current quarter; the interest of customers and partners in them is quite high. The announcement of the Instinct MI350 family of accelerators is scheduled for the second half of 2025, and the debut of the Instinct MI400 with CDNA Next architecture is scheduled for 2026.

AMD’s net profit in the third quarter more than doubled to $771 million. The company’s profit margin increased year-over-year from 47 to 50%. Operating expenses increased by 15% to $1.96 billion. The other “ray of light” in AMD’s quarterly report, not counting the server segment, was the client segment. In this area, the company managed to increase revenue by 29% to $1.9 billion. Ryzen processors with Zen 5 architecture were in good demand, as noted in AMD’s presentation. Operating profit in the customer segment nearly doubled to $276 million, and operating profit margin rose from 10% to 15%. As noted in the company’s documentation, it expects to introduce the next generation Ryzen 9000 X3D processors in the fourth quarter of this year, before the end of November. The launch of Ryzen 9000 processors allowed the company to increase revenue by double-digit percentages in the third quarter.

The gaming segment did not please with its dynamics, since the demand for components for the current generation Sony and Microsoft game consoles was naturally declining. As a result, AMD’s revenue in this area at the end of the third quarter decreased by 69% to $500 million, operating profit shrank from $208 to $12 million, and the operating profit margin dropped from 14 to 2%. As Lisa Su explained, in the Radeon video card segment, revenue decreased in the third quarter in anticipation of the release of new graphics processors with RDNA 4 architecture, which will be introduced in early 2025.

The embedded solutions segment reduced its quarterly revenue by 25% year-over-year to $927 million. The company notes that its customers continue to develop previously accumulated product inventories. AMD’s operating profit in this segment decreased from $612 to $372 million, and its operating profit margin dropped from 49 to 40%.

It is important that AMD management raised its forecast for revenue in the artificial intelligence systems segment from $4.5 to $5 billion for the entire 2024 year. The turnover of the entire industry will grow to $500 billion by 2028, growing by an average of more than 60% annually. Demand for computing accelerators not only drove up revenue in the server segment, but also raised the company’s profit margin. For the current quarter, AMD expects to generate between $7.2 billion and $7.8 billion in revenue and maintain a profit margin of 54%.