Seasonal demand for products based on NAND flash memory in the second half of 2024 was weaker than expected, which led to a decrease in contract prices for wafers with such chips in the third quarter. This downward trend is expected to intensify, with prices falling by more than 10% in the fourth quarter, analyst firm TrendForce reports.

Image source: samsung.com

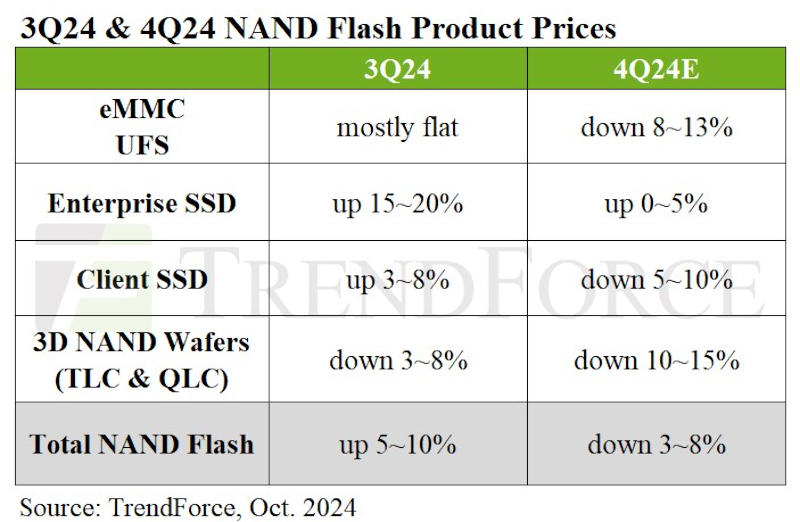

The only segment that is likely to see modest price increases is enterprise SSDs, with contract prices projected to rise 0-5% in the fourth quarter. For UFS and PC SSDs, customers will adopt more cautious purchasing strategies as end-product sales will be weaker than previously expected. As a result, overall contract prices for NAND memory will decrease by 3-8%.

Although manufacturers are aggressively rolling out sales of AI-powered PCs, inflation and little practical innovation in AI will keep consumers from rushing out to buy new PCs. Several large manufacturers returned to full capacity in the third quarter, and others increased production by upgrading processes, but stable demand in the server segment is not enough to support price increases given the sluggish consumer market. An additional headwind is the widening gap between spot market prices, supply chain prices and OEM contract prices. As a result, contract prices for consumer SSDs for PCs in the fourth quarter will decrease by 5-10%.

Image source: trendforce.com

Smartphone and laptop makers have adopted a strategy of reducing inventory, leading to more conservative NAND memory orders. But suppliers continued to ramp up production, leading to oversupply. The smartphone market showed no signs of recovery in Q3 as many manufacturers depleted eMMC supplies and resisted price hikes, leading to limited contracts. New models from a number of Chinese brands have brought new impetus to the eMMC market, but all of them will likely try to avoid building up excess inventory. In the third quarter, there was a prolonged price confrontation between suppliers and buyers – suppliers increased inventories in the module market and on the spot market, which tipped the scales in favor of buyers. As a result, contract prices for eMMC will decrease by 8–13%.

In the UFS memory market, which is used mainly in premium and flagship smartphones, the situation is similar to the situation in the eMMC market. Due to the weak economic dynamics, smartphones began to be replaced not once every two years, as before, but once every three years, and there was no breakthrough in the market that could turn the situation around. As a result, contract prices for UFS in the fourth quarter will also decrease by 8–13%.

Retail demand for client SSDs, memory cards and USB drives has remained modest since early 2024. Seasonal sales ahead of the end of school holidays and holidays in Europe and the USA failed to stir up consumer interest; Due to the economic slowdown in China, demand is expected to weaken during the trade festival on November 11 – these factors are likely to further exacerbate the decline in demand for NAND wafers in the fourth quarter. Module manufacturers continue to be left with excess inventory, and suppliers have had to switch to a price-cutting strategy to remain operational. As a result, contract prices for NAND wafers could decline by 10-15% in the fourth quarter, TrendForce warns, and if market conditions worsen further, a more serious decline is possible.