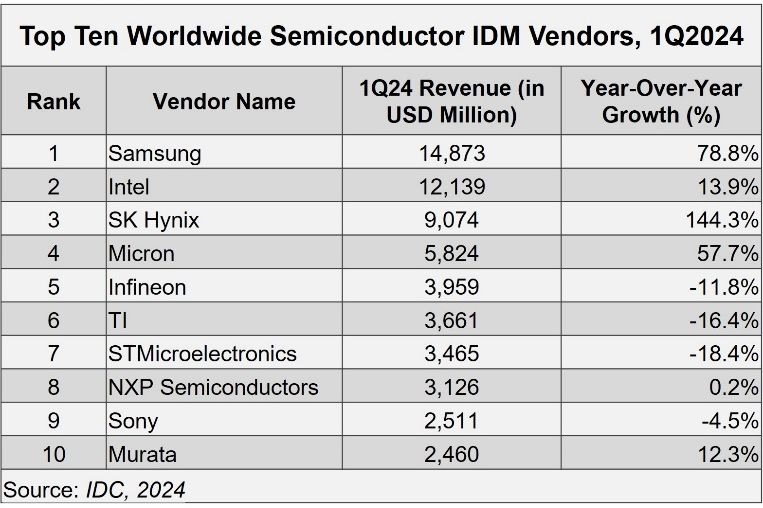

It’s no secret that in the context of the artificial intelligence boom, memory manufacturers are becoming one of the main beneficiaries, along with developers of chips for computing accelerators. In the first quarter, SK hynix increased its revenue by 144.3%, which allowed it to become the third largest chip manufacturer, Intel still holds the second position, and the first was taken by Samsung Electronics, which increased its revenue by 78.8%.

Image Source: Samsung Electronics

The fact that Samsung for a long time could not obtain certification for compliance of its HBM3 and HBM3E memory chips with Nvidia requirements for components for modern computing accelerators does not negate Samsung’s ability to supply its HBM memory of other generations for the needs of all market participants. Secondly, the recovery in demand for memory generally had a positive effect on Samsung’s revenue in the first quarter, and therefore it grew by 78.8% to $14.9 billion.

Image source: IDC

IDC experts note that high prices for HBM chips also contributed to accelerated revenue growth for memory manufacturers. Compared to DRAM of the classical layout, HBM chips are four or five times more expensive, and the reorientation of DRAM production lines to HBM production has additionally contributed to the rise in prices for conventional DDR. Ultimately, memory manufacturers benefited from these trends. The top five largest chip manufacturers at the end of the first quarter included three memory manufacturers, including Micron, which took fourth place and showed revenue growth of 57.7% to $5.8 billion. In monetary terms, memory manufacturers received half of the total revenue of the ten largest chip manufacturers. IDC statistics include companies that themselves both develop and produce semiconductor products.

In general, the needs of the computing solutions sector accounted for 35% of the revenue of the ten largest chip manufacturers in the first quarter; over the year, this share increased by six percentage points. Next comes the telecommunications solutions segment. The automotive segment is now trying to prevent warehouse overstocking, as a surge in activity in this area after shortages caused by the pandemic has encountered a slight cooling in demand. It is possible that the automotive segment, combined with the market for industrial automation components, will show some recovery in demand in the third quarter, as IDC representatives explain. Throughout this year, the leading positions in the IDM market in terms of revenue dynamics will be occupied by memory manufacturers, according to IDC experts.