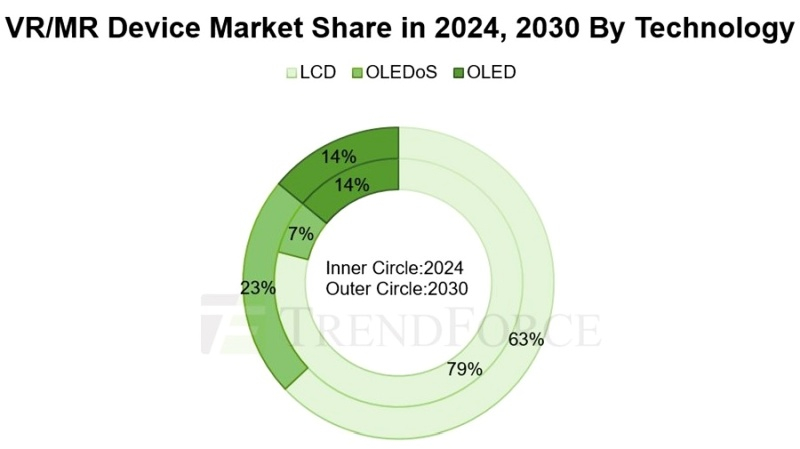

According to analytics firm TrendForce, display shipments for mixed reality (MR), augmented reality (AR) and virtual reality (VR) devices will grow over the next few years as current inventory sells out. OLEDoS-based microdisplays are expected to dominate high-end devices, capturing up to 23% of the market by 2030, while LCDs will account for 63% of mid-range devices.

Image source: TrendForce

TrendForce predicts that shipments of VR headsets and similar devices could reach 37.3 million units by 2030, with a CAGR of 23% from 2023 to 2030. Sony and Apple’s collaboration to create the Vision Pro headset has made OLEDoS the dominant technology in the high-end VR/AR headset market.

OLEDoS (OLED on Silicon) is an innovative display with a diagonal size of less than 1 inch and an ultra-high resolution of over 3000 pixels per inch. Unlike conventional OLED displays based on glass and polyamide substrates, OLEDoS uses CMOS substrates based on silicon wafers used in the production of chips and image sensors.

Displays created using this technology are distinguished by their low weight and thickness, as well as high uniformity of characteristics. TrendForce notes that CMOS manufacturing complexity and lower yield rates result in high manufacturing costs for OLEDoS displays, which has limited penetration growth for now.

Chinese manufacturers such as SeeYa and BOE are actively involved in the production of OLEDoS. This is expected to facilitate rapid penetration of this technology in the VR/MR device market by reducing costs. OLEDoS has high potential in the high-end headset market, with TrendForce believing its market share will increase from 7% in 2024 to 23% in 2030.

LCD technology continues to dominate VR/AR devices, not least due to Meta✴’s focus on cost-effectiveness. However, as demands for higher resolution and image quality increase, 1200 ppi LCD products will face competition from other technologies. TrendForce estimates that shipments of such displays will total 6.8 million units in 2024, down 5.6% from 2023.

TrendForce experts note that LCD technology still has room for further modernization, for example, increasing resolution beyond 1500 pixels per inch. With a major manufacturer such as BOE continuing to actively develop the production of LCD displays for VR/MR devices, TrendForce believes that LCD technology will remain highly competitive in the mid- and low-end market, and by 2030 the share of such displays will be 63%.

TrendForce notes that conventional OLED technology is inferior to OLEDoS in quality, and LCD – in cost. Additionally, the adoption of OLED in the VR/AR headset market is highly dependent on specific manufacturers. TrendForce estimates that OLED’s share of this segment will remain between 13% and 15% from 2024 to 2030.