For Intel management, the current quarterly report was a big test, since the company had to cut costs and headcount, and revenue dynamics could not please investors. By voicing the need to save money amid falling revenues, the company unwittingly caused its stock price to drop nearly 19% in the after-hours of trading, to less than $24 a share.

Image source: Intel

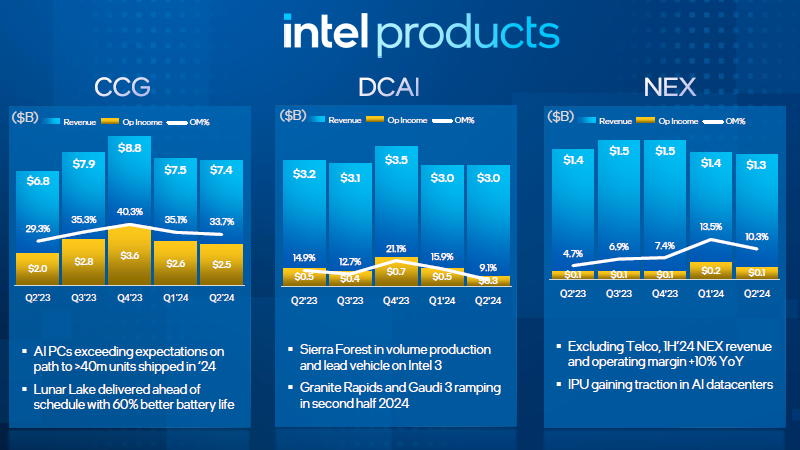

Actually, the “lesser evil” in this situation was a decrease in the company’s revenue by 1% year-on-year to $12.8 billion. This is lower than the $12.94 billion forecast by analysts, which was an additional disappointment for investors. While a year ago the company ended the quarter with a net profit of $1.48 billion, the second quarter of this year brought it a net loss of $1.61 billion. CEO Patrick Gelsinger tried to attribute the losses to the company’s desire to bring it to market faster Core Ultra processors of the Lunar Lake family, which meet the current requirements of Copilot+ PC and provide a 60% increase in laptop battery life compared to their predecessors. Gelsinger is convinced that it was worth it, as the AI PC segment is expected to grow to more than 50% of the PC market by 2026 from its current 10% share of the PC market. Intel’s profit margin dropped from last year’s 45.8% to 38.7% in the last quarter. The company’s management said it launched a program to significantly reduce production costs in response to unfavorable market conditions.

Secondly, Intel decided to quickly move the production of chips using Intel 4 and Intel 3 technologies from the experimental line in Oregon to a plant in Ireland. CFO David Zinsner explained that this will increase the company’s costs in the short term, but will improve profit margins in the future. Another factor that worked against Intel in the second quarter was the “more competitive pricing environment in the market.” This means that AMD and Qualcomm made efforts to attract buyers of Intel products in their respective market segments.

The attempts made by the previous management of Intel to reduce the company’s dependence on the PC segment after Patrick Gelsinger took office were considered inappropriate; at the end of the last quarter, the segment brought the company 58% of all revenue. In dynamics, this meant that Intel’s revenue from the sale of PC components increased year-on-year by 9% to $7.42 billion and almost coincided with experts’ expectations. Specifically in the AI PC direction, the quarterly results turned out to be higher than Intel’s own forecasts; the company is still confident in its ability to supply more than 40 million PCs with the necessary processors at the end of the current year, although so far it has only completed 15 million. By the end of 2025, this number should exceed 100 million units accumulated total. Shipments of Core Ultra processors more than doubled in the past quarter in a sequential comparison. Intel’s profit margin in the client segment dropped from 35.3% to 33.7% over the year.

Intel promises to launch Arrow Lake desktop processors in the next quarter, which will offer AI acceleration features in this segment.

In the server segment, the company’s revenue decreased by 3% year-on-year to $3.05 billion, falling below the $3.14 billion forecast by analysts. Intel’s presentation notes that processors of the Sierra Forest family are mass-produced and are the leading type of products manufactured using Intel 3 technologies. In the second half of the year, the company expects to begin scaling the production of Granite Rapids processors and computing accelerators of the Gaudi 3 family.

Intel’s cost-cutting plan for the next year and a half, in addition to staff reductions, involves reducing research and acquisition costs from the current $20 billion to $17.5 billion. This year, the company’s capital expenditures will fall within the range of $25 to $27 billion, which is 20 % less than the previous level, next year the limits will drop to $20–23 billion. However, Intel expects to finance up to half of these amounts through partners and subsidies, so its own capital expenditures will not exceed $13 billion this year and $14 billion next year. In total, this year Intel is going to save up to $20 billion in operating expenses; next year, the amount of savings will be limited to $17.5 billion, but in 2026 it will exceed this value. Previously, Intel expected to spend 20% more in 2025.

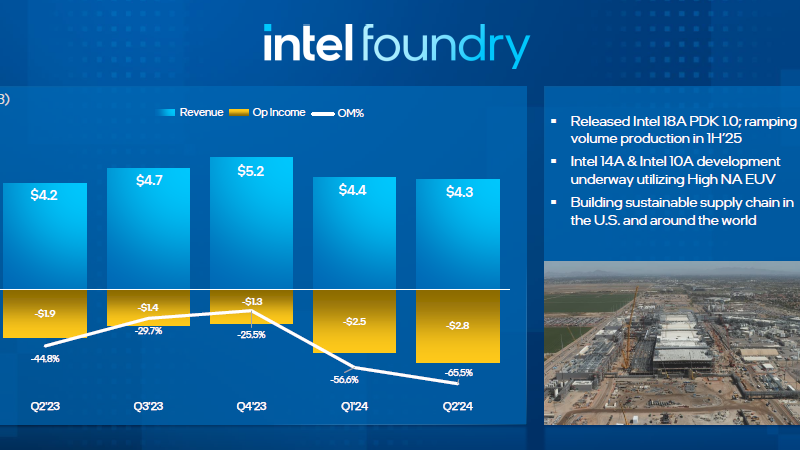

The Intel Foundry division, which is responsible for producing products for both the parent corporation itself and for third-party clients, increased its revenue year-on-year by 4% to $4.3 billion, while operating losses increased from $1.4 to $2.8 billion. More than 85% of silicon wafers processed by Intel are produced using technologies that do not involve the use of so-called EUV lithography, and this negatively affects production costs.

The company expects to begin production of products using the latest Intel 18A technology in the next half of the year, thereby fulfilling the goal of mastering five new technological processes in four years. Gelsinger hopes that Intel Foundry’s financials will bottom out this year and then turn a profit. Intel Foundry’s services business will be led by Kevin O’Buckley, and the division’s manufacturing operations will be led by newly appointed Naga Chandrasekaran, formerly of Micron Technology. The company will begin supplying processors using Intel 18A technology only next year.

The company plans to introduce Panther Lake client processors that will be produced according to these lithographic standards in the second half of 2025. Panther Lake samples are already allowing test systems based on them to boot Windows. This family of processors will be the first to use a RibbonFET transistor structure, power supply from the reverse side of the PowerVIA wafer, and an advanced spatial layout. The appearance of these processors will symbolize the return to the Intel assembly line of more crystals included in its own processors. Current Intel chips are more dependent on TSMC services for chip manufacturing. Intel 14A and Intel 10A technologies will use High-NA EUV lithographic scanners. The company will begin producing chips using Intel 20A technology in serial quantities starting from the next quarter.

In the third quarter of this year, Intel expects revenue from $12.5 to $13.5 billion, which is $850 million below market expectations at the top end of the range. At the very least, the company expects revenue growth in the server segment in the second half of the year due to seasonal factors. However, demand in the client and server segments is not meeting Intel’s own expectations, especially in China, and the concentration of server segment spending on AI solutions, which the company does not have, is causing it to lower its forecasts for the corresponding areas of activity this year. Intel management expects that the company’s market position will not weaken significantly this year. The profit margin will be 38% based on the results of the third quarter.

Contrary to tradition, Intel management gave a forecast for the fourth quarter. Counting on the market recovery after overstocking, it assumes that the company’s revenue growth in the fourth quarter of this year will reach 5% on a sequential basis.

At the beginning of the next quarter, Intel is going to suspend dividend payments, which is quite logical in the current situation. In total, Intel aims to save up to $10 billion by 2025 while still being able to make investments that impact the company’s long-term performance.