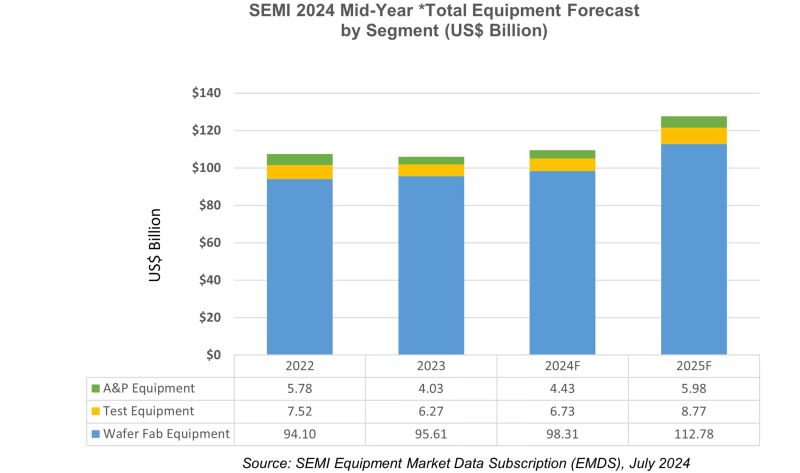

According to the SEMI association, the volume of supplies of equipment for the production of semiconductor components in monetary terms at the end of the current year will increase by 3.4% to a record $109 billion. Next year, the growth rate will even increase to 17%, and a new revenue record will be fixed at $128 billion , thanks in large part to the boom in artificial intelligence systems.

As SEMI recalls, another record was achieved last year in the form of $96 billion in revenue from the sale of equipment for the production of semiconductor components for silicon wafer processing plants. This year, there will be an increase in revenue in this area by 2.8% to $98 billion. At the end of last year, SEMI representatives expected that revenue in this area at the end of 2024 would be limited to $93 billion, but six months later the forecast was improved. This was facilitated by both the high activity of Chinese chip manufacturers and the restoration of demand for DRAM and HBM memory chips. According to SEMI representatives, next year revenue from the sale of equipment for silicon wafer processing enterprises will increase by 14.7% to $113 billion. This will be facilitated not only by the high growth in demand for memory chips, but also by the demand for advanced technological processes used for the production of logic components.

After two years of contraction, chip testing and packaging equipment will show revenue growth in the second half of this year. Directly, revenue from the sale of equipment for testing chips will grow for the entire year by 7.4% to $6.7 billion, and in the segment of equipment for chip packaging, a 10% increase in revenue will increase it to $4.4 billion. Next year, revenue growth rates will increase: up to 30.3% in the segment of equipment for testing chips, and up to 34.9% in the segment of equipment for packaging them. This will be driven by both increased demand for components with complex spatial layouts and the recovery in demand for chips in the automotive, industrial and consumer segments. In addition, projects planned for this period for the construction of new enterprises will also make their feasible contribution.

Image source: SEMI

The distribution of dynamics across market segments this year will not be uniform. Thus, equipment for the production of logic components and in the contract direction will reduce supplier revenue by 2.9% to $57.2 billion compared to 2023. This will be driven by lower demand for equipment used in combination with mature technical processes, as well as the “high base” for comparison formed in the advanced lithography segment last year. In 2025, this equipment segment will show growth in production by 10.3% to $63 billion. This will be facilitated by growing demand for products manufactured using advanced lithography, as well as the planned expansion of production capacity.

This year, costs for memory production equipment will increase the most. If in the NAND segment growth this year is limited to 1.5% to $9.35 billion, then next year core revenue will increase by 55.5% to $14.6 billion. The DRAM segment, which includes HBM, will demonstrate growth in revenue from the sale of specialized equipment by 24.1%, and in the next year it will be limited to 12.3%.

The geographical cross-section of the forecast demonstrates relative stability in the interval up to 2025 inclusive. The leading consumers of chip production equipment will remain China, Taiwan and South Korea, with the PRC remaining the undisputed leader. This year it will purchase a record $35 billion worth of chip production equipment, increasing its lead over other regions. If in some geographic areas these expenses will decrease this year and then increase next year, then for China the next year will be characterized by a decrease in purchases after three years of active spending on related needs.